Excerpt:

When payroll is handled by an external third-party service, maintaining financial accuracy in QuickBooks requires manually recording all expenses, deductions, and tax liabilities. The most precise method for both QuickBooks Online and Desktop is through creating Journal Entries that strictly adhere to double-entry accounting principles. This involves mapping external data to at least five custom Chart of Accounts, including specific expense accounts (Wages, Employer Taxes) and liability accounts (Federal and State Taxes). For effective reconciliation and audit readiness, users must separate Gross Wages, Net Wages, and all tax components, often using a Payroll Clearing Account to manage fund flow and timing differences. Additionally, QuickBooks Desktop users must utilize the Setup YTD Amounts window for accurate entry of historical tax payments made prior to using the software.

Highlights (Key Facts & Solutions)

Overview

Payroll is the compensation a company should pay to its employees for a specified period of time or on a given date. These days, payroll is usually outsourced to third-party service providers who perform a wide range of payroll-related tasks. The payroll includes different processes such as creating a list of paid employees, tracking their working hours, calculating pay, providing their salary on time, employee benefits, tax withholding, audit and reporting, creating and maintaining records, etc.

Small business owners can pay and manage their teams with integrated payroll, and access HR, health benefits, and more. QuickBooks payroll software also includes same-day direct deposit and automatic tax filing, which is backed by tax penalty protection. To ensure financial accuracy, it’s essential to record payroll expenses, deductions, and tax liabilities correctly in QuickBooks, even when processed elsewhere.

If you’ve already paid taxes outside QuickBooks Online Payroll but it’s still showing as a tax due on your payroll product, you need to record such payments. Here’s how to record tax payments made for prior tax periods, or payments made outside of QuickBooks Online Payroll.

Record your tax payment

If the payments are not listed:

If you need to edit a prior payment:

In QuickBooks Desktop Payroll, you can enter historical tax payments that you’ve made during the current or previous years before using the payroll service.

QuickBooks Desktop uses this information to determine how much you still owe to federal and state agencies and to ensure that your future tax deposits and filings are accurate. Below are the two ways to enter it.

Note: The process of figuring out what you still owe requires research into your liabilities and payment amounts. To enter tax payments properly, print and carefully review the Tax Payments Checklist and consult with your accountant. Also, provide them a copy of the Tax Payments checklist so that they understand the payroll setup requirements of this task.

If you are trying to enter historical tax payments for the current year or previous years, you can use the Payroll Setup window.

Let’s see how:

You can use the backdoor process if you’re trying to enter historical tax payments for the current or previous years.

Follow these steps:

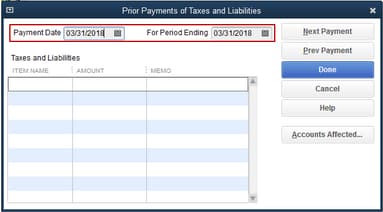

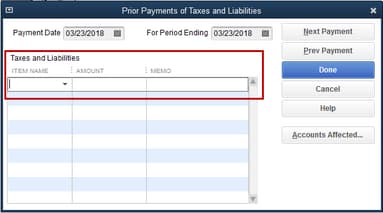

Note: If there is already an item with an amount selected under Taxes and Liabilities, press Next Payment. This may be a prior payment that you have already entered.

If you use QuickBooks for accounting and another service to run payroll, you still need to keep track of those paychecks in QuickBooks. We call paychecks made outside of QuickBooks with services like ADP or Paychex third-party paychecks.

Some payroll services allow you to import paycheck data directly into QuickBooks. However, if your service doesn’t have this feature, we’ll show you how to manually track these payments as journal entries. This keeps your payroll and account data all in one place.

If you haven’t already, follow the steps to create new accounts in your Chart of Accounts to track your payroll liabilities and expenses.

Create these expense accounts. Select Expense as the account type:

Create these liability accounts. Choose Liabilities as the account type:

Note: These accounts cover the most common payroll tax-related scenarios. You may need to create additional accounts for taxes specific to your state or locality.

Once you pay your employees outside of QuickBooks, create a journal entry.

To create the journal entry, you need to use the info from your payroll report. If you paid multiple employees for the pay period, you can combine all of their paycheck totals into one journal entry. You can also create separate journal entries for each employee if you need to break out the details.

Add Gross Wages

Add Employer Payroll Taxes

Note: You can combine the following taxes into one debit, or add each tax item as separate debits: Social Security Employer, FUTA Employer, Medicare Employer, State Job training taxes and State unemployment insurance.

Add Taxes Paid Towards 941 or 944 Taxes

Note: You can combine the following taxes into one debit, or add each tax item as separate debits: Federal Income taxes, Social Security Employee, Social Security for Employer, Medicare for Employee, and Medicare for Employer

Add State Unemployment Insurance Taxes

Note: You can combine the following taxes into one debit, or add each tax item as separate debits: State Unemployment Insurance and State Employment Training Tax

Add State Income Taxes

Note: You can combine the following taxes into one debit, or add each tax item as separate debits: State Personal Income Tax and State Disability Insurance.

Add Federal Unemployment Taxes (FUTA)

Add Net Wages

You can still use the Manual Payroll feature even with the existing payroll service to enter prior year paychecks. For this, let’s set up a manual payroll first.

Here’s how:

Once done, enter your payroll manually by following these steps:

You can create a journal entry to enter your employees third-party payroll information. Let’s first make sure to create the necessary expense accounts used to track your payroll liabilities and expenses.

Here’s how:

You can repeat the same steps to create all the necessary accounts for each payroll income, deduction, contribution and liabilities.

Once completed, you can now create a journal entry to record your employee’s deductions, contributions and liabilities.

When payroll is processed outside of QuickBooks, most businesses struggle with incomplete entries, tax mismatches, and inaccurate reports. This section breaks down five key areas that are often overlooked but critically important for maintaining clean books and staying compliant. Whether you’re manually entering data or reconciling third-party reports, these focused topics will help you avoid costly errors, streamline your accounting, and ensure your payroll records are audit-ready.

Using third-party payroll affects at least three key financial areas: expense classification, tax liability accuracy, and bank reconciliation. If not recorded properly, payroll expenses may be understated by 15–20%, especially when employer taxes and benefits are missed. Additionally, tax payments made by the provider must be logged to avoid duplicate liabilities in your books. Reports become unreliable if gross pay, deductions, and net pay aren’t matched with your chart of accounts. At month-end, reconciliation gaps often arise due to this disconnect. You must map every external payroll entry correctly to maintain compliance, transparency, and audit readiness.

Manual payroll entries must be mapped to at least five account types: wages, taxes, benefits, liabilities, and bank accounts. Incorrect mapping leads to imbalanced books, tax errors, and compliance issues. Each paycheck includes gross wages, employer taxes, and employee deductions—all must hit specific accounts. For example, missing “Payroll Liabilities” can cause overstated expenses by 10–25%. QuickBooks relies on the Chart of Accounts to generate accurate reports, so every journal entry must align with these categories. With clear mapping, you gain financial clarity, reporting accuracy, and year-end simplicity—key for audits, planning, and tax filing.

Multi-state payroll adds three major layers of complexity: varying tax rates, state-specific liabilities, and unique deduction rules. If journal entries don’t reflect state-level breakdowns, you risk underreporting liabilities by 20–30%. Each state may have its own unemployment tax, disability insurance, or training contributions, which must be tracked through separate liability accounts. Using a single generic account can collapse your compliance framework. To avoid penalties, ensure each state’s tax is logged correctly in the Chart of Accounts. This approach enables precise reporting, clean audits, and legally compliant filings across all jurisdictions where employees reside or work.

Most businesses make three recurring mistakes: combining net pay with gross, ignoring employer taxes, and skipping liability accounts. These errors distort profit margins by up to 18% and lead to inaccurate tax filings. Another major slip is recording lump sums without separating wages, benefits, and taxes, making reconciliation nearly impossible. Also, using incorrect dates—like check date instead of pay period end—can misalign cash flow reporting. To stay accurate, always break down payroll entries line-by-line, match accounts, and verify totals. Avoiding these mistakes ensures financial precision, audit safety, and seamless month-end close without cleanup surprises.

Reconciling payroll involves matching three core components: net pay, tax payments, and benefit deductions with actual bank transactions. If journal entries don’t align with these, your books can show false liabilities or missing expenses—often off by 5–10% per payroll cycle. Many overlook timing differences, like delays in tax debits, causing reconciliation mismatches. Always cross-check each paycheck’s net pay against bank outflows and ensure taxes are recorded on the date they clear. Accurate reconciliation gives you clean financials, real-time cash flow insight, and full audit traceability, which is essential for both internal reviews and external audits.

Recording payroll outside QuickBooks is just one part of the equation—managing it smartly is what keeps your books clean and compliant. This section provides five high-impact insights that enhance the efficiency, accuracy, and legal standing of your external payroll process. From setting up the right accounts to preparing for in-house migration, these topics are designed to help you build a robust system that scales with your business. Whether you’re a small team or a growing company, these strategies will ensure your payroll data is not only recorded—but recorded right.

Recording payroll through journal entries offers three major advantages: full control over account mapping, flexible customization for third-party data, and streamlined reconciliation. Unlike automated systems, manual entries allow you to separate wages, taxes, and benefits clearly—improving transparency and reporting accuracy. They also let you backdate entries, which helps correct past periods without altering live payroll. For businesses using providers like ADP or Paychex, this method ensures data alignment, tax compliance, and clean integration into QuickBooks. With journal entries, you’re not dependent on imports or sync errors—just clear, traceable, and organized financial records.

A payroll clearing account acts as a temporary holding space for payroll-related transactions, ensuring accurate cash tracking, cleaner reconciliations, and reduced errors. Set it up as a bank-type account in your Chart of Accounts and use it to route net wages, tax liabilities, and benefit deductions during journal entry creation. As payments are made, this account helps you match journal entries with actual bank activity, avoiding discrepancies. It’s especially useful when third-party providers process payments on different schedules. A clearing account ensures transparency, control, and real-time accuracy without cluttering your main checking or payroll accounts.

Before switching to in-house payroll, complete a 3-step checklist: verify prior liabilities, gather YTD payroll data, and audit tax payments. Missing any step can cause duplicate taxes, compliance gaps, or incorrect employee balances. Start by collecting all third-party reports, including wage summaries, tax filings, and benefits deductions. Next, reconcile those figures with your QuickBooks records to spot inconsistencies. Finally, update your Chart of Accounts to reflect manual control over payroll entries. This preparation ensures your transition is smooth, your data is accurate, and your first in-house payroll run is error-free, compliant, and audit-ready.

To stay compliant, you must align three critical elements: reported wages, tax liabilities, and payment timelines. Errors in external payroll entries can trigger IRS notices, penalties, or interest up to 25% of the unpaid amount. Every journal entry must reflect accurate amounts for Federal Income Tax, Social Security, Medicare, and state-specific taxes like SUI or SDI. Late or missed recordings may also result in inaccurate W-2s or 941 filings. Regular audits, matched liability accounts, and reconciled payment dates ensure full regulatory compliance, clean tax records, and zero surprises during year-end reviews.

Integrating payroll summaries into your monthly close process ensures accurate financials, faster reconciliation, and cleaner reporting. Use payroll reports from your third-party provider to validate wages, tax payments, and benefit deductions against your QuickBooks journal entries. A mismatch as small as 2–5% per month can distort profit and loss statements and delay close timelines. Always compare totals with your expense and liability accounts before finalizing books. This integration helps detect errors early, supports accrual adjustments, and delivers audit-ready, tax-compliant financial statements—every single month.

When recording payroll processed outside of QuickBooks, you’re recommended to follow a structured approach to ensure accuracy and compliance with financial records. By manually entering payroll expenses, liabilities, and tax with holdings, you can maintain precise payroll records and meet various laws, regulations, and legal obligations, such as withholding the correct amount of taxes and providing accurate wage statements.

It provides a comprehensive overview of the financial transactions associated with employee payments, such as wages, salaries, bonuses, overtime, and benefits. Choosing third-party service providers to streamline your payroll-related tasks, including reporting, tax filings, and compliance, can be beneficial for businesses with complex payroll regulations.

To accurately reflect the complex nature of payroll using a journal entry, you must create and map the external payroll data to at least five specific account types in your Chart of Accounts.

These accounts separate expenses, liabilities, and assets:

Incorrect mapping or combining these categories will lead to imbalanced books and inaccurate tax reports.

The basic rule of double entry accounting must be followed to ensure the journal entry balances and correctly impacts your financial statements.

Payroll taxes and liabilities (both employee and employer portions) are also credited to the respective liability accounts, increasing the amount the business owes before the tax payments are recorded.

A Payroll Clearing Account acts as a temporary holding account, typically set up as a bank-type account, to isolate the movement of payroll funds.

Using a clearing account provides three major advantages:

The danger of combining net pay with gross wages or ignoring employer taxes is that it causes your financial statements to be highly inaccurate, leading to compliance risk.

The three primary errors that result are:

Before creating the final journal entry in QuickBooks, you must reference the payroll summary report from the external service (ADP, Paychex, etc.) to capture specific, separate totals.

The elements you must extract and enter as separate lines are:

If you skip separating employer taxes and employee withholdings, you cannot map the correct amounts to the required liability accounts.

The “backdoor” process (Ctrl + Alt + Y or Ctrl + Shift + Y from the Help menu) is used in QuickBooks Desktop to enter historical tax payments (Year-to-Date or YTD amounts) made before the business began using the QuickBooks Payroll service.

The specific reasons for using this method are:

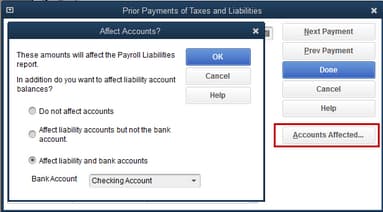

When recording historical tax payments outside the standard flow in QuickBooks Desktop, the user sees options for how the payment affects the Chart of Accounts (COA).

The “Do not affect accounts” option is chosen under specific circumstances: