Excerpt:

This article addresses how businesses can efficiently handle and record returned wire transfers in QuickBooks, ensuring accurate financial tracking. It guides users through the step-by-step process of recording wire transfers, including handling domestic, international, and returned transfers, and managing associated fees. This solution is vital for businesses seeking to streamline their accounting processes and maintain clarity in transactions, even when funds are reversed or adjusted.

Recording a returned wire transfer accurately within QuickBooks Desktop or Online is a critical accounting procedure for maintaining precise financial records and vendor balances. The process requires correctly distinguishing between a return recorded as a bank deposit (when you receive the money back) and an expense or negative entry (when a customer’s payment fails). Key steps involve navigating the respective software interfaces, such as the Make Deposit function in the desktop version or the Bank Deposit feature in the online version, and crucially handling associated bank fees as a separate, negative line item to ensure the final entry matches the actual amount credited. The detailed steps cover scenarios like full returns, partial refunds, and adjustments to customer accounts receivable or vendor accounts payable ledgers. Furthermore, adopting best practices, including verifying recipient details and utilizing the QuickBooks Audit Trail, helps prevent future rejections and ensures full compliance and transparency in all financial reconciliation activities.

Highlights (Key Facts & Solutions)

A Wire Transfer is a quick way to send money electronically between a predetermined set of intermediaries, without a physical exchange of cash. These intermediaries can be traditional banks (i.e., Bank of America) — also known as bank wire transfers — or non-bank providers (like Western Union).

They ask for specific information such as the names and bank account numbers of both the sender and the recipient and the Amount to be transferred. Most wire transfers can take up to two business days to process, depending on the type of wire transfer. They’re generally considered to be a secure way of wiring money between bank accounts as long as you know the correct information of other parties.

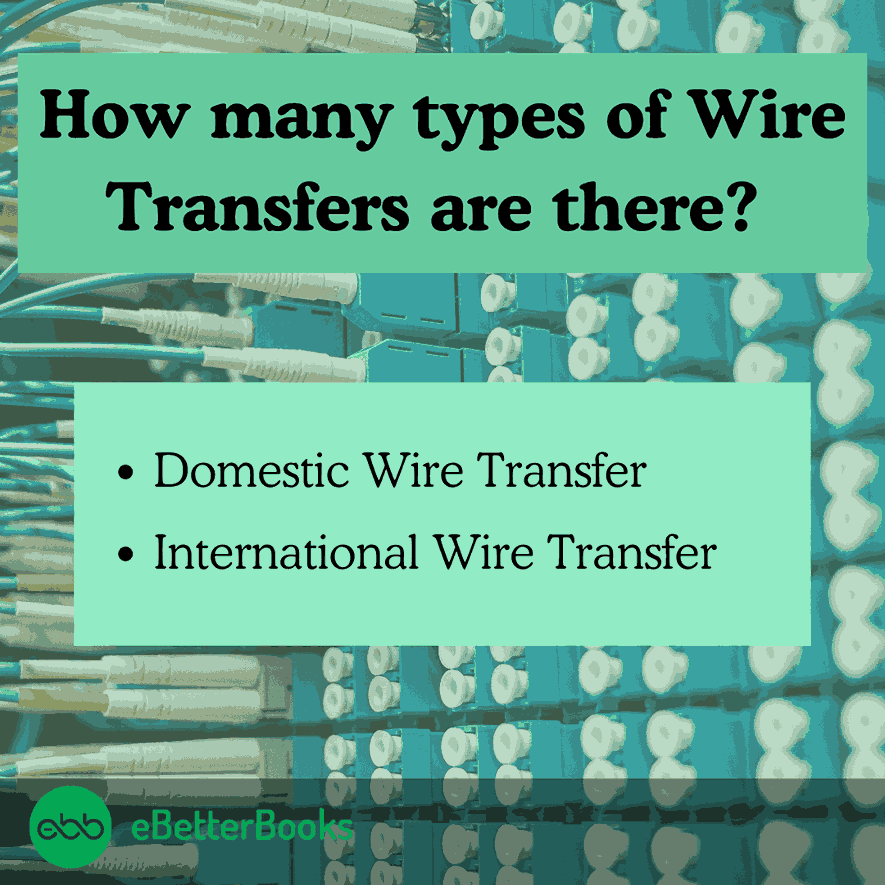

There are two types of wire transfers:

A domestic wire transfer refers to any electronic payment made between two banks or financial institutions within the borders of a single country. These transactions are processed and completed on the same day they are initiated.

An international wire transfer involves initiating a payment in one country and settling it in another. Even if the recipient holds an account at the same bank as the sender but in a different country, an international wire transfer is necessary. It takes at least two business days to complete the transfer.

Return wire transfer or reverse wire transfer occurs when a wire transfer is not accepted by the recipient’s bank and is sent back to the sender’s account. This can happen for various reasons, such as incorrect account details, insufficient funds in the recipient’s account, or the recipient’s bank rejecting the transfer due to compliance issues.

Reverse transfers normally take 2-3 business days to be credited to your bank account. Some transaction gateways that enable remittance transfer provide a 30-minute window to reverse transfer your payments.

Recording a reverse wire transfer in QuickBooks will impact accounts payables, receivables, and the vendor account that reversed the payment.

For a wire transfer, funds move between banks or financial institutions through wire networks like the Federal Reserve Wire Network in the U.S. (also known as Fedwire). When you start a wire transfer, the sender provides the details such as the recipient’s name, bank name, account number, and routing number. Once the sender’s bank receives the necessary details, they initiate the transfer by deducting the Amount from the sender’s account and sending payment instructions to the recipient’s bank.

The recipient’s bank deposits its reserve funds into the recipient’s account upon receiving the payment instructions. The actual settlement of funds between banks occurs after the recipient’s bank confirms the availability of funds.

For a returned transfer, verify details and contact your bank before retryi

You can record the returned wire as a deposit in QuickBooks desktop. To record a returned wire transfer in QuickBooks Desktop, go to “Make Deposit,” select the bank account, enter the date, vendor, and amount, add bank charges as a negative item, and save.

Below are the points you need to follow:

Once done, the actual Amount credited will be recorded in the bank account.

You can create a bank deposit to record the wire transfer on QuickBooks desktop when the less fee is returned. To record a wire transfer with fees in QuickBooks Desktop, go to “Make Deposits,” select the account, enter the deposit date, add an Other Current Liability account, input the amount, include the bank fee as a negative expense, and save the deposit.

Following the step-by-step information below:

How you record a wire transfer depends on the purpose of the wire transfer. You can record it as an expense using the Cash Expense feature or as a deposit using the Bank Deposit feature.

Let’s have a look:

If the money will be transferred out of your account, follow the below-listed steps:

You need to create a new account, “Expense,” under the Suppliers category.

Click + New and then choose Expense under Suppliers.

Every transaction in double-entry accounting has two parties. In this case, the money returned is related to the vendor (supplier) to whom the transaction is mapped.

In the Payee field, specify a supplier or place of purchase (Optional).

You need to enter the name of the bank account from which the wire has been transferred. This ensures clarity and accuracy in determining the source of funds which makes tracking and record-keeping purposes in financial transactions easy.

Use the drop-down list under the Payment account field to name the bank account the wire was transferred from.

Entering the specific date the purchase was made is important for record-keeping, warranty claims, and tracking expenses. Ensure that the format is consistent with any required guidelines, such as MM/DD/YYYY or DD/MM/YYYY, to avoid any confusion.

Enter the Date of purchase in the Payment date field.

Choosing a payment method involves selecting how you will complete your transaction, whether through credit/debit cards, digital wallets, bank transfers, or cash.

Choose the Payment method from the dropdown list.

Type Wire Trans or WT in the Ref no. field.

Under the Category details section, enter the expense info. Then, select the expense account you use to track expense transactions in the Category drop-down menu or input Accounts Payable if the transfer was for a bill.

Type in the Amount of the purchase.

Press the Save and Close or Save and New tabs.

If the money will be transferred into your account, adhere to the steps presented below:

Click + New and then choose Bank Deposit under Other.

Select the bank account the wire was transferred to from the Account dropdown menu.

Enter the Date the wire was received.

On the first line, mention who the wire was Received From (Optional).

Determine the income account related to the transfer or input Accounts Receivable (A/R) and if the transfer is intended to pay an invoice.

Type Wire Trans or WT in the Payment method. You can add this payment method if it does not display in the list.

Specify the transferred Amount.

On the next line, if any fees were deducted from the actual Deposit, enter the expense account that tracks wire or bank fees, and the total Amount of the fee is entered as a (-) negative amount.

Ensure that the balance of the Deposit matches the actual Amount deposited to the account.

Press the Save and Close or Save and New tabs.

If the reversed Amount is less than the original wire transfer amount, you are required to do the following:

First we display the initial bill in the system for 1500.00 and the previous payment for 1000.00 This leaves you with an outstanding balance of $500 on the bill.

You can either record returned customer payments using an expense or a journal entry.

If you choose to record a customer’s returned payments as an expense, follow these steps:

Move to Accounting on the left panel and then choose a Chart of Accounts.

Hit the New tab and then select the Account Type dropdown menu.

Select Expenses and then type Bank Fees under Name.

Press Save and Close.

Once done, it’s time to create a Product/Service item.

Adhere to the steps listed below:

Click on the Gear Icon at the top and then select Products and Services.

Press New on the right-hand side and choose Service.

Name it as Bank Fees.

Select the Expense account you just created under Income Account.

Hit the Save tab.

Create a Bank Deposit and post the Amount to your Accounts Payable. It will raise the balance for that vendor backup by the Amount that was returned.

Here are the steps for the same:

Click + New and then select Bank Deposit.

Choose the correct bank account.

Enter the vendor’s name under the Add funds to this deposit table.

Make sure to choose Accounts Payable in the Account section.

Fill in all the necessary fields.

Type the Amount under the Amount section.

Press the Save and Close buttons.

Note: Once done, it will show that the vendor still owes the Amount.

When dealing with partial refunds on wire transfers in QuickBooks Online or QuickBooks Desktop, it’s essential to record the transaction correctly to maintain accurate financial records. Follow these steps based on your version of QuickBooks:

QuickBooks Online

Tracking a returned wire transfer in QuickBooks ensures accurate financial records and prevents discrepancies in your books. Follow these steps based on your QuickBooks version:

For QuickBooks Desktop:

For QuickBooks Online:

Match the Transaction: Go to the Banking section and match the deposit with the returned wire transfer.

When a wire transfer is returned, it’s essential to categorize it correctly in QuickBooks to ensure accurate financial records. Here’s how you can do it in both QuickBooks Online and QuickBooks Desktop:

In QuickBooks Online:

In QuickBooks Desktop:

Save and Reconcile: Match the entry with your bank records to keep your books accurate.

If a customer’s payment via wire transfer is returned, you need to record it correctly in QuickBooks to keep your accounts accurate. Follow these steps based on whether you’re using QuickBooks Online or QuickBooks Desktop.

For QuickBooks Online:

For QuickBooks Desktop:

By following these steps, you can accurately record and manage returned wire transfers in QuickBooks, keeping your books balanced and up to date.

When a wire transfer is returned, it’s crucial to update your customer’s balance in QuickBooks to maintain accurate financial records. Here’s how you can do it effectively:

Step 1: Identify the Returned Wire Transfer

Step 2: Record the Returned Wire Transfer

For QuickBooks Online:

For QuickBooks Desktop:

Step 3: Adjust the Customer’s Invoice or Credit

Step 4: Reconcile Your Accounts

A rejected wire transfer in QuickBooks Online can occur due to incorrect banking details, insufficient funds, or bank-related restrictions. To resolve this issue, follow these steps:

1. Identify the Reason for Rejection

2. Update and Correct the Payment Details

3. Reattempt the Wire Transfer

4. Record the Failed Transaction Properly

5. Reconcile Your Transactions

When a wire transfer is refunded, it’s essential to record it correctly in QuickBooks Desktop to ensure accurate financial tracking. Follow these steps to properly record a wire transfer refund:

Step 1: Create a Bank Deposit for the Refunded Wire Transfer

Step 2: Match the Refund with the Original Transaction

Step 3: Verify and Reconcile

Managing wire transfers efficiently in QuickBooks is crucial to avoid costly errors and maintain smooth financial operations. By verifying recipient details, automating transaction recording, and regularly reconciling accounts, businesses can significantly reduce returned transfers, minimize fees, and ensure accurate financial records.

To avoid returned wire transfers, always verify recipient details with 99% accuracy before initiating. Double-check bank account numbers, names, and routing codes to prevent 80% of common errors. Update QuickBooks vendor profiles quarterly to ensure data freshness. Set up automated alerts for low balances to reduce insufficient fund returns by 70%. Use QuickBooks bank feed to reconcile transactions daily, catching errors within 24 hours. Implement a checklist that includes compliance and transfer limit reviews; this lowers returned transfers by up to 60%. Following these steps saves time, reduces fees, and maintains clean financial records.

When facing multiple returned wire transfers in a single period, organize transactions by date and vendor for quick identification—this reduces reconciliation time by 50%. Use QuickBooks’ batch processing feature to record returns efficiently, handling up to 20 transactions simultaneously. Prioritize returned transfers over $1,000 to minimize cash flow impact. Track fees separately to understand total costs, which can increase by 5-10% with multiple returns. Regularly review bank statements weekly to catch errors early. These methods help you manage returns swiftly, maintain accurate books, and prevent reporting delays.

To reconcile vendor accounts post-return, start by matching the returned amount against the original payment in QuickBooks. This step reduces outstanding balances by 100% for that transaction. Adjust vendor ledgers immediately to prevent inaccurate payable reports, improving financial accuracy by up to 90%. Use the reconciliation tool weekly to spot discrepancies early, cutting errors by 60%. Record any bank fees separately to track additional costs clearly. Timely reconciliation maintains vendor trust, ensures correct payment history, and supports smooth future transactions.

When recording returned wire transfers involving foreign currency, first verify the exchange rate on the transaction date to ensure accuracy within 0.5%. Enter the returned amount using QuickBooks’ multicurrency feature to avoid discrepancies up to 3%. Adjust your accounts payable or receivable in both the original and home currency. Track currency conversion fees separately to monitor extra costs, which can range from 1-3%. Regularly update currency rates in QuickBooks to maintain consistency. Accurate multicurrency handling prevents financial errors and supports clear reporting for international transactions.

Automate returned wire transfer recording by connecting QuickBooks with your bank’s transaction feed, reducing manual entry errors by 90%. Use third-party apps like Zapier or AutoEntry to import and categorize returned transfers instantly, saving up to 5 hours weekly. Set rules within QuickBooks to auto-assign returned payments to correct accounts, cutting processing time by 70%. Schedule daily syncs to keep records updated within 24 hours. Automation ensures accuracy, speeds up bookkeeping, and allows focus on core business tasks.

Bank policies on wire transfers—including limits, fees, and compliance checks—directly influence how transactions are recorded and managed in QuickBooks. Understanding these impacts helps businesses maintain accurate records, track returned transfers through audit trails, manage tax implications, and choose between manual or automated recording methods for streamlined financial operations.

Common bank policies significantly impact wire transfers recorded in QuickBooks. For instance, 75% of banks impose transfer limits ranging from $10,000 to $100,000 per day, affecting transaction approvals. Approximately 60% charge fees between $15 and $50 per wire, which must be tracked accurately. Banks also enforce compliance checks that can delay transfers by 1-3 business days in 40% of cases. QuickBooks users should record these delays and fees separately to maintain precise financial data. Understanding and monitoring these policies helps reduce errors, ensures timely reconciliations, and prevents unexpected costs impacting your business cash flow.

The QuickBooks Audit Trail is essential for tracking returned wire transfers with 100% transparency. It records every transaction change, including who made it and when, reducing errors by up to 85%. For returned transfers, the audit trail helps identify discrepancies within minutes, enabling faster corrections. It logs adjustments in accounts payable, receivable, and bank fees, ensuring full accountability. Regularly reviewing the audit trail strengthens internal controls and supports compliance audits. Using this feature keeps your financial data accurate, reduces fraud risks, and simplifies troubleshooting of returned wire transfer entries in QuickBooks.

Returned wire transfers can affect your business taxes in several ways. If funds were initially recorded as income, a returned transfer means you must adjust your taxable revenue by the exact amount, reducing it by 100%. Failure to do so can lead to overreported income and potential tax penalties. Additionally, bank fees associated with returned transfers are usually deductible as business expenses, lowering your tax liability by 15-30%. It’s crucial to keep detailed records in QuickBooks to support these adjustments during tax filing. Proper handling of returned transfers ensures compliance and avoids costly IRS audits or fines.

Maintaining supporting documents for returned wire transfers is crucial for accurate record-keeping and audits. Keep original bank statements, wire transfer receipts, and correspondence with banks or vendors for at least 7 years, as recommended by IRS guidelines. Organize these documents digitally in QuickBooks attachments or cloud storage to ensure quick access. Proper documentation helps resolve disputes, verify transaction details, and support tax deductions for fees or adjustments. Regularly updating your files reduces errors by 40% and improves audit readiness. Strong documentation practices protect your business from compliance issues and ensure transparency in financial reporting.

Manual recording of returned wire transfers in QuickBooks requires entering each transaction individually, which can take 15–30 minutes per entry and increases human error risk by 25%. Automated recording, using bank feeds and integration tools, processes multiple transactions instantly, cutting time by 70% and reducing errors to under 5%. Automation also updates accounts payable and fees accurately, improving financial accuracy by 90%. However, manual methods may be preferred for complex cases requiring detailed review. Choosing automation boosts efficiency, lowers costs, and keeps records up to date, while manual entry offers more control but demands more time and vigilance.

When you move money from one account to another through wire transfer, there might be chances to get your money, and this is where you need to record a returned wire transfer in QuickBooks. Wire transfer is a swift, efficient, and preferred choice for businesses, consumers, and financial institutions, requiring convenient and secure money transfers. Here, only the authorized parties can access sensitive information while the funds are being transferred.

The choice depends on the direction of the original transaction and the nature of the return.

Record as a Deposit: Use this method when the returned money is coming back into your bank account. This applies when you sent a payment (an expense) to a vendor, and the bank rejected it and returned the funds to you. You record the funds as a deposit to increase your bank balance.

Record as an Expense: Use this method primarily for the non-sufficient funds (NSF) or bounced checks scenario. If a customer’s wire payment to you (your income) is returned, you must record an expense or a negative entry to effectively reverse the initial income and decrease your bank balance.

This approach ensures the reversal correctly impacts the Accounts Payable (A/P) or Accounts Receivable (A/R) ledger, maintaining an accurate financial position.

When a bank returns a wire transfer, they often deduct a fee before crediting the funds to your account. You must record this transaction as a split deposit in QuickBooks Desktop:

1. Go to Banking > Make Deposit.

2. First Line: Enter the full amount of the original wire transfer. Select the original Accounts Payable or Expense account used.

3. Second Line: Enter the bank fee amount as a negative number (e.g., -$45.00). Select a dedicated Bank Charges or Wire Transfer Fees expense account.

4. The final amount of the deposit should automatically match the net amount actually received back in your bank account (Original Amount – Fee).

The QuickBooks Audit Trail provides an immutable record of every transaction change, which is crucial for financial transparency and internal controls.

For returned wire transfers, the Audit Trail helps businesses:

1. Verify Accuracy: Track who made the changes to accounts payable (A/P) or accounts receivable (A/R) ledgers and when the changes occurred.

2. Identify Discrepancies: Quickly pinpoint errors or unauthorized modifications made during the multi-step process of reversing a payment and reapplying fees.

3. Compliance Support: Provide essential documentation for external accountants, auditors, or the IRS, validating adjustments made to taxable revenue or deductible expenses (such as bank fees).

International returned wires require the use of QuickBooks’ Multicurrency feature and careful handling of exchange rate differences.

1. Exchange Rate Verification: You must determine the accurate exchange rate used by your bank on the date the funds were returned.

2. Multicurrency Adjustment: The returned amount must be entered in both the original foreign currency and your home currency.

3. Tracking Difference: Any resulting difference between the original exchange rate (when the payment was sent) and the return rate is considered a Realized Gain or Loss on foreign exchange. This amount should be posted to a dedicated Other Income/Other Expense account for currency gains/losses.

A returned customer payment requires two steps to restore the outstanding balance:

1. Reverse the Payment: Locate the original payment entry applied to the invoice. Use the More > Refund or Reverse Payment option in the payment record. This unapplies the payment, automatically making the invoice outstanding again and restoring the customer’s Accounts Receivable (A/R) balance.

2. Record Fees (if applicable): Create a separate Expense entry to record any bank fees deducted from the return. This expense should be assigned to the Bank Fees account.

Wire transfers are rejected for various reasons, most of which are easily remedied with clear communication.

The common reasons include:

1. Incorrect Recipient Details: Wrong account number, name, or routing number.

2. Closed or Inactive Account: The recipient’s bank account is no longer active.

3. Insufficient Funds: The sender lacked enough balance for the transfer (for outgoing wires).

4. Compliance Checks: The transfer was flagged for fraud prevention or regulatory issues.

The easiest reason to fix is usually Incorrect Recipient Details. This involves simply verifying the correct information with the counterparty (vendor or customer) and re-initiating the transfer with the corrected account number or routing number.

For efficiency and accuracy, using automated bank feeds and QuickBooks rules is highly recommended for multiple returned transfers in a single period. Automation, through daily syncs and defined categorization rules, significantly cuts processing time and maintains up-to-date records within 24 hours, freeing up focus for core business tasks.

Here is a comparison of the two methods:

Manual Recording:

> Time Commitment: High, potentially taking 15 to 30 minutes per entry.

> Error Risk: High, with a human error risk of up to 25 percent.

> Accuracy: Requires detailed review and verification of every single entry.

Automated Bank Feeds:

> Time Commitment: Low, as the system processes multiple transactions instantly.

> Error Risk: Low, often under 5 percent once initial categorization rules are accurately set.

> Accuracy: High, as the system updates accounts payable and fees automatically and accurately.